Risk and reward sharing is a simple and attractive concept, offering a commissioner the opportunity to co-opt and incentivise a provider to moderate growth in healthcare demand by sharing in the savings or cost over-runs. The Centers for Medicare and Medicaid Services (CMS), a US government agency, has established a comprehensive approach to risk and reward sharing for US Accountable Care Organisations: the Shared Savings Program. This paper draws out the central themes from the Shared Savings Program and translates these into an NHS context.

The rationale that underpins the development of Accountable Care Organisations in the US and Integrated Care Systems in England is similar: to moderate healthcare costs through service coordination and integration. However, US ACOs and English ICSs are vastly different in scale (on average, US ACOs provide services to c. 19,000 enrolled patients) and operate in radically different political, financial and cultural contexts.

In the US, ACOs are required to sign up to one of three risk-sharing ‘tracks’. Track 1 is a one-sided risk-sharing model where providers have the potential to share in savings if priced activity falls below expected levels, but are not required to pay a share of any cost over-runs. Tracks 2 and 3 are two-sided models, exposing providers to an increasing proportion of upside and downside risks. Six years since the first ACOs were established more than 90% of ACOs remain on track 1. This suggests that to date, providers have a limited appetite for risk. It also offers some insight into the level of confidence that US ACOs have in their ability to moderate demand growth.

Complexity is a key feature of any robust risk-reward sharing arrangement and is likely to increase transaction costs above those associated with fee-for-service arrangements. The complexity arises as the commissioner or system designer attempts to ensure that the incentives accurately reflect the policy intention, and do not instead reward cost shunting, quality reductions or chance variations in costs.

It is possible to extend risk-reward sharing to multiple partners within an Integrated Care System and to organisations outside the scope of an ICS. But these extensions add further complexity.

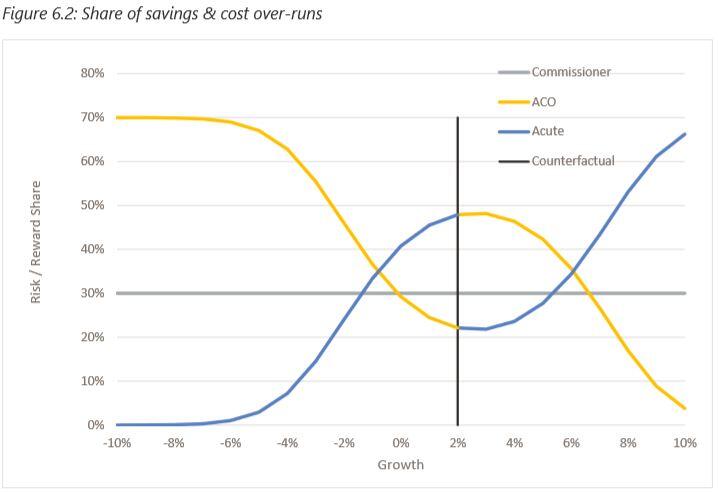

The notion of a ‘counterfactual’ is central to risk-reward sharing. In this context a counterfactual is the price of healthcare activity that might be expected under normal circumstances. It is the benchmark against which priced activity levels are assessed at year end. If priced activity falls below this level, then the provider may be entitled to a reward payment. If it exceeds this level, then a penalty may be applied. There are many approaches to calculating and agreeing counterfactuals, but none are simple. These calculations determine the allocation of significant sums of money.

If the NHS is to make best use of risk and reward sharing, then it must be aware of the complexities and hazards inherent in these arrangements as well as the potential benefits.

If you would like to contact us about this work or about any ways we might help you in addressing the issues raised, please use the form below.